CCME.NEWS, covering the regional and global HVACR industry with an unwavering commitment to providing in-depth news and analyses on policy, business and technology

On January 21, we conducted the 5th Edition of Refrigerants Review, and once again, the topic of training of technicians came up for discussion in the context of indiscriminate venting of refrigerants, at a time when global attention has intensified on preventing refrigerant-instigated climate change. Nabil Shahin of AHRI MENA and Markus Lattner of Eurovent Middle East spoke for long and with palpable passion about the urgent need for making technicians fall in line. A detailed report on the conference will appear in the February issue of the magazine, but Nabil and Markus set off a tsunami of thoughts on persistent gaps in the industry that cannot wait from being highlighted.

Surendar Balakrishnan

Those gaps do not have to do only with refrigerants. It is sad to say, but we are faced with gaping holes in almost every identified action point, be it relating to energy efficiency, Indoor Air Quality (IAQ) or food security – inadequate cold chain-related food losses in the post-harvest stage and the consequential emission of methane from landfills. We are confronted with idiosyncrasies and numerous instances of numbing complacency, dithering, indecisiveness, being in denial, working at cross purposes, refusing to factor in indispensable interventions at the time of budgeting, wallowing in myths and jettisoning facts for sheer convenience – even when they are staring us in the face.

It is not just poor technician behaviour, but also poor leadership behaviour. Pulling out of multilateral agreements is just one example of leadership deficit. Failure to tighten codes that need urgent updating, failure in enforcement, failure in surveillance and showing a willingness to prioritise the superficial over the profound are all examples of a collective leadership failure and an unfortunate short-term mindset.

I could be inaccurate, but about the only area that draws a certain urgency is the data centre sector. There, we get to see intensity of thought and action and a greater political will and response, simply because that is where the money is. Indeed, a strong commercial interest and the knowledge that data centre equipment will carry out the threat of failing, if not treated properly, and taking down with them data worth millions, causes the most unflappable of leaders to break into cold sweat. And that’s because the stakes are too high – any disruption and its consequences will attract lawsuits and repercussion, with no escape door for accountability.

So, it is all about a real and perceived danger with an unambiguous, direct cause-and-effect equation that goads leaders into action. Which means, there has been a collective communication failure in firmly establishing this cause and effect in the realms of energy efficiency, IAQ and other equally mission-critical aspects. You may choose to argue otherwise – and you are entitled to your opinion – but temporary patching up won’t do. We need to see single-minded focus and a certain ruthlessness to pull society away from the abyss.

Premium Story

Empower highlights continued focus on national talent development in District Cooling

Company says investment in national human resource development remains a core pillar of its strategic vision

DUBAI, UAE, 27 January 2026: Empower has announced that it maintained the Emiratisation levels in its workforce by the end of 2025, reflecting its commitment to developing national human capital and empowering Emirati talent across sectors.

Making the announcement through a Press Release, the company said its learning and development programmes have contributed to strengthening the presence of UAE nationals across engineering, technical and administrative roles, adding that this has enhanced their contribution to the organisation’s growth and sustainability efforts. Empower said it has also reaffirmed its commitment to providing a work environment that supports diversity, inclusion and gender balance, noting that Emirati women now account for 46% of its national workforce compared to 54% Emirati men.

H.E. Ahmad Bin Shafar

H.E. Ahmad Bin Shafar, CEO, Empower, said: “This approach embodies the vision of our leadership, which places people at the forefront of development priorities, and reflects the company’s commitment to operating under a clear, long-term strategy focused on building and developing national competencies capable of effectively contributing to leading the future of the sustainable District Cooling sector. At Empower, we are keen to empower our national workforce and equip them with advanced knowledge and skills that support their professional growth and enhance their ability to innovate and contribute to achieving growth and sustainability objectives.”

H.E. Bin Shafar added that “Empower places great importance on strengthening the presence of national competencies across various technical, engineering, and administrative roles in the District Cooling industry, stemming from our belief in their pivotal role in achieving operational excellence. With qualified Emirati hands, we continue to consolidate Empower’s position as a leading model in investing in national human capital and contributing to supporting the country’s direction toward a more sustainable future for generations to come.”

Empower said investing in the development of national human resources is a core pillar of its strategic vision. The company added that it continues to implement specialised training and development programs aimed at enhancing the capabilities of Emirati employees, strengthening their readiness to keep pace with sector requirements and supporting the growth of the District Cooling industry in line with the UAE’s vision for a sustainable, knowledge- and innovation-driven economy.

Andrew Schumer, Founding Partner and CTO, Darklake, speaks on the need for turning data into control

Andrew Schumer

Most HVAC systems are still managed reactively. Components break, performance drops or energy costs rise; and teams respond. By that point, comfort has already been affected, and money has already been wasted. Digital twin technology changes this approach.

A digital twin is a live operational model of an HVAC system built on real data. It continuously captures temperature, airflow, pressure, energy use and equipment condition. Instead of relying on static designs or delayed alarms, operators see how systems are behaving in real time.

This visibility allows problems to be identified early. Common issues, such as valve degradation, refrigerant loss, sensor drift or fan inefficiency, can be detected before they lead to failure. Maintenance becomes planned rather than urgent, downtime is reduced and asset life is extended.

Digital twins also reduce risk when changes are required. Seasonal demand shifts, control strategy updates and equipment upgrades can be tested virtually before being applied to live systems. Teams can see the impact on comfort, energy consumption and system stability in advance. This leads to better decisions and fewer costly errors.

Energy performance improves, as well. Setpoints and control logic can be continuously adjusted based on actual operating conditions. Buildings use less energy while still meeting comfort and sustainability requirements.

As HVAC systems become more connected, security becomes part of operational reliability. Integration with building management systems, IoT sensors and cloud platforms increases exposure. A compromised HVAC system can become an entry point into wider networks.

Darklake delivers HVAC digital twin solutions with security built in from the start. By combining accurate system modelling with cyber resilience, monitoring and segmentation, Darklake ensures intelligent HVAC systems remain efficient, reliable and safe to operate.

The real value of smarter HVAC is control you can trust.

Nabil Shahin of AHRI MENA says the rise of geothermal heat pumps is being driven by sustainability mandates and incentives

Geothermal heat pumps (GHPs) have come a long way since they were first introduced in the US market somewhere around the late 1970s. What used to be viewed as somewhat of an alien concept by many homeowners has grown more mainstream, and is expected to globally reach USD 12 billion by 2033, driven by sustainability mandates, incentives and consumer demand for energy efficiency.

In the US, ground-source geothermal heat pumps (GSHPs) remain a small but growing share of new construction, estimated at 2-5% of new homes in 2024. That figure was about 0.5 per cent 20 years ago. Many factors have contributed to the growth, including more consumer awareness of the benefits of geothermal, increased demand for energy efficiency and the need for reducing the carbon footprint among consumers, technological improvements, more experience on the part of dealers and installers, high-quality training opportunities and government incentives for homeowners.

Types of geothermal heat pumps

GHP efficiencies have gone up dramatically. Some of the technology improvements include variable-speed fan motors, variable-speed or two-stage compressors and advanced controls. These all have led to increased comfort, better dehumidification and quiet operation.

There are four basic types of ground loop systems. Three of these – horizontal, vertical and pond/lake – are closed-loop systems. The fourth is the open-loop option. Which one of these is best depends on the climate, soil conditions, available land and local installation costs at the site. All of the approaches can be used for residential and commercial building applications.

Horizontal system

This type of installation is generally most cost-effective for residential installations, particularly for new construction where sufficient land is available. It requires trenches at least four feet deep. The most common layouts either use two pipes, one buried at six feet, and the other at four feet, or two pipes placed side-by-side at two metres in the ground in a one-metre-wide trench. The proprietary Slinky method of looping pipe allows more pipe in a shorter trench, which cuts down on installation costs and makes horizontal installation possible in areas it would not be with conventional horizontal applications.

Vertical system

Large commercial buildings and schools often use vertical systems, because the land area required for horizontal loops would be prohibitive. Vertical loops are also used where the soil is too shallow for trenching, and they minimise the disturbance to existing landscaping. For a vertical system, holes – approximately 10 cm in diameter – are drilled about six metres apart and 30-120 metres deep. Into these holes go two pipes that are connected at the bottom with a U-bend to form a loop. The vertical loops are connected with a horizontal pipe (manifold), placed in trenches, and connected to the heat pump in the building.

Lake/water body

If the site has an adequate water body, this may be the lowest cost option. A supply line pipe is run underground from the building to the water and coiled into circles at least 2.5 metres under the surface to prevent freezing in cold regions and excessive heat in hot regions. The coils should only be placed in a water source that meets minimum volume, depth and quality criteria.

Open-loop system

This type of system uses well or surface body water as the heat exchange fluid that circulates directly through the GHP system. Once it has circulated through the system, the water returns to the ground through the well, a recharge well or surface discharge. This option is obviously practical only where there is an adequate supply of relatively clean water, and all local codes and regulations regarding groundwater discharge are met.

Benefits of GHPs

The biggest benefit of GHPs is that they use 25%–50% less electricity than conventional heating or cooling systems. This translates into a GHP using one unit of electricity to move three units of heat from the earth. According to the US Environmental Protection Agency (US EPA), geothermal heat pumps can reduce energy consumption and corresponding emissions by up to 44% compared to air-source heat pumps and up to 72% compared to electric resistance heating with standard air conditioning equipment. GHPs also improve humidity control by maintaining about 50% relative indoor humidity, making GHPs very effective in humid areas.

Today’s geothermal systems, using the Earth’s natural energy, can heat and cool a home, and provide domestic water heating, as well. They also can be used in combination with radiant floor heating systems, including systems integrated with solar panels, and can also provide heating for snow-/ice-melting and pools. The US EPA touts GHPs as one of the “most efficient and comfortable heating and cooling technologies currently available” and estimates that ENERGY STAR-qualified GHPs use about 30% less energy than standard heat pumps. How much a homeowner can save in energy costs by installing a geothermal system will depend on the type of equipment to which it is being compared.

Other considerations

Upfront cost: Geothermal systems in residential applications have higher installation costs, but the payback period is typically 3-7 years, due to energy savings and incentives.

Longevity: Geothermal systems last longer – 20-25 years for the unit, 50+ years for the ground loop – than conventional systems, which typically last 10-15 years.

High-ambient temperature (HAT) regions: Since GHPs are primarily used for cooling in HAT regions, they are constantly dumping heat underground. Therefore, it may be necessary to use larger trenches or a greater number of boreholes, as heat dissipation could become an issue, unlike in climates where both heating and cooling are required, and the system extracts heat from underground during heating, resulting in a more balanced thermal exchange throughout the year.

Key AHRI standards for geothermal

The main AHRI standard for geothermal heat pumps is AHRI 870 for “Performance Rating of Direct Geoexchange Heat Pumps”, and the related AHRI 871 (for SI units). These standards define the technical requirements and rating conditions for performance testing and certification of direct geoexchange (DGX) systems, which are used in programmes like ENERGY STAR. There are also standards for other types, such as AHRI 600 for Water-Source Heat Pumps and AHRI 1300 for Commercial Heat Pump Water Heaters that use geo-exchange.

The writer is Managing Director of AHRI MENA. He may be reached at NShahin@ahrinet.org

Premium Story

Sotirios Papathanasiou joins as Advisor to “IEQ & Fertility” campaign

Widely recognised for his contribution to air quality-related education, Papathanasiou has the ability to translate intricate technical and environmental data into actionable insights

DUBAI, UAE, 26 January 2026:Climate Control Middle East magazine appointed Sotirios Papathanasiou as an official Advisor to the Editorial Campaign, “IEQ & Fertility”. The campaign aims to bridge the gap between Indoor Environmental Quality (IEQ) and reproductive health, highlighting how air quality impacts human life at its most fundamental level.

Sotirios Papathanasiou

Papathanasiou joined the campaign with a distinguished background in electronics engineering and environmental advocacy. He is the founder of “GO AQS” and “See The Air”, and is regarded as a globally recognised voice in air quality education, and for the ability to translate intricate technical and environmental data into actionable insights for the general public.

“We are thrilled to welcome Sotirios to this vital campaign,” said Surendar Balakrishnan, Editor of Climate Control Middle East, and Co-Founder & Editorial Director of CPI Industry. “His unique blend of technical mastery in sensing technologies and his deep commitment to public health communication makes him an invaluable asset. As we explore the profound connection between the air we breathe and fertility, Sotirios’ analytical rigour and market foresight will ensure our message is scientifically sound and widely accessible.”

Papathanasiou’s involvement as an advisory expert in various international air quality initiatives further strengthens the campaign’s mission to advocate for healthier indoor environments across the Middle East and beyond.

Premium Story

Epta to showcase refrigeration solutions at EuroShop 2026

Company says its presence at the retail trade fair will focus on immersive experiences, integrated solutions and live discussions addressing key industry topics

MILAN, Italy, 23 January 2026. Epta announced its participation at EuroShop 2026, which it said is taking place in Düsseldorf from 22 to 26 February 2026. Making the announcement through a Press Release, Epta said it will exhibit in Hall 15 at Booth B24–B42 and said it will present what it describes as a new generation of all-round commercial refrigeration solutions. Epta added that the exhibition space has been designed as a gateway for retailers to explore new possibilities through the Group’s portfolio and what it terms conscious innovation.

Epta said its offering is based on its New Product Development approach, which it said focuses on consciousness, uniqueness, flexibility and trustworthiness, and added that the models on display demonstrate the integration of technology, design and services to enable what the company describes as tailored and increasingly high-performance solutions.

Sharing his vision of the company’s presence at this year’s event, Aurélien Tissot, Marketing Senior Director, Epta Group, said: “EuroShop 2026 will be the ideal stage to highlight Epta’s role as a Fully Integrated Solutions Provider, capable of supporting retailers during the entire lifecycle of their stores, in their transition towards long-term sustainability and in the development of smarter, more distinctive and profitable store formats.”

Epta said its exhibition will feature a reimagined experiential journey supported by digital and multimedia content, and added that these tools are intended to encourage dialogue with its experts and foster networking. Epta also said it will host live discussions at the booth through the Talking Epta Arena, bringing together retail leaders, opinion leaders, industry associations, partners and customers to share insights on daily key topics for the sector.

Tissot said: “In a market that never stops evolving, innovating and anticipating the needs of its consumers, Epta helps its customers to stay ahead, offering a new generation of solutions designed to turn fresh areas into hot spots unlocking new levels of value creation. For Epta, real progress doesn’t stop at ‘done’, but keeps moving forward, fueled by responsibility, curiosity and collaboration. A shared effort that is made possible by the contribution of more than 8,000 EptaPeople and by the trust of customers and partners in line with our purpose, ‘Preserving our Planet with Conscious Innovation. Together.’”

Epta said it will also host a press conference at its booth for the first time, where the Group’s top management will present its current profile, market positioning and strategic priorities and outline its vision for the future of retail.

Dr Rajendra Shende says the world must move from debate to delivery

Dr Rajendra Shende

The Amazon, widely considered the lungs of the world, witnessed a peculiar autopsy in its own dissection room, Belém, at COP30. The global community opened its own failure of meeting the target of limiting the rise in the planet’s temperature to 1.5 degrees C above pre-industrial levels. This diagnosis, delivered with grim finality by UN Secretary-General, António Guterres before the talks even began, was based on global observations produced by the World Meteorological Organization (WMO). He stated that an overshoot of this temperature is now inevitable. The planet clearly is in a critical condition. Unfortunately, the doctors that gathered for COP30 were still debating over the basic design of the cure.

When COP30 convened in Belém, in November 2025, the host nation, Brazil labelled the Summit as the “COP of Implementation”, “People’s COP” and “a COP of truth”. The Brazilian Presidency went far in creating the ambience and ecosystem of ‘Global Mutirão: Uniting humanity in a global mobilisation against climate change. The Presidency’s work was not only challenging but also breathtaking!

Indeed, when measured against past conferences, COP30 did make progress. When measured against the physics of climate change, however, the gathering revealed an uncomfortable reality: While climate diplomacy is becoming more refined, the pace of real-world transformation remains dangerously slow. For industry and government leaders, the question is no longer whether COPs deliver agreements but whether those agreements are structurally capable of driving the scale and speed of change needed.

Negotiations make progress but expose excuses

One of the clearest signals from COP30 was the collective acknowledgement that the era of abstract negotiations has failed the planet. Guterres was unusually direct in his pre-COP and closing statements, noting that incrementalism is incompatible with a world that is already overshooting the temperature limits of the Paris Climate Agreement. His message was echoed across analyses by expert media – the tools exist, capital is available and the technologies are mature; what remains deficient is political follow-through.

Emphasising on renewed Nationally Determined Contributions (NDCs) as delivery mechanisms rather than diplomatic artefacts

Spelling out clearer timelines for the mobilisation of climate finance through the New Collective Quantified Goal (NCQG) on climate finance from developed countries

Linking the operational progress on adaptation, and loss and damage

Yet, the absence of enforceable consequences for delay or non-compliance continues to hollow out ambition. And the fact that even at the end of COP30, fewer than half of the countries had submitted updated 2025 NDCs, even after extended deadlines, to address the overshoot of warming, exposed cracks in political will and reinforced failure in governance. Those NDCs are needed to rebuild the lost forts, to remain below 1.5 degrees C.

Climate Finance, a necessary step forward, still insufficient

COP30 did deliver tangible progress on climate finance, particularly in setting a clearer pathway towards the long-promised scale-up beyond the USD 100 billion benchmark to USD 300 billion by 2035. Developing countries welcomed the operationalisation of the Loss and Damage Fund and the agreement to triple adaptation finance to USD 120 billion per year; observers cautiously endorsed the development.

The shift from abstract pledges to more structured mobilisation pathways was needed. However, as multiple post-COP assessments noted, the timing remains misaligned with need. Adaptation finance, in particular, continues to lag behind escalating climate impacts. Delaying scale-up targets by even five years translates to lost productivity, damaged assets, health crises and rising humanitarian costs – expenses that ultimately return to public budgets and balance sheets.

Finance without urgency and timely delivery has now become a climate liability.

The Global Cooling Pledge: Progress that risks becoming unequal

One of COP28’s most notable initiatives was the launch of the Global Cooling Pledge, positioned as a response to escalating heat stress, particularly in rapidly urbanising regions. Recognising cooling as essential infrastructure – not a luxury – is a forward-looking breakthrough. Heat already kills more people annually than floods, storms and cold combined, and productivity losses from extreme heat are mounting sharply; yet, the framing of the pledge reveals a critical imbalance.

The dominant narrative around cooling at COP30 focused heavily on urban design, buildings and city-level resilience. These are important priorities, but a cooling agenda that concentrates primarily on cities in middle- and high-income countries risks reinforcing ‘just transition’ and global inequity.

For large parts of Africa, South Asia and fragile states, cooling is not about comfort, as experienced in the urban habitat; it is about:

Food preservation in agricultural value chains,

Vaccine and medicine storage in overstretched health systems,

Safe working conditions for labour-intensive economies and productivity, and

Human survival during heatwaves that already exceed physiological thresholds

Treating cooling predominantly as an urban planning or architectural challenge overlooks its role as a foundational enabler of development. A ‘just transition’ cannot prioritise cooling for offices and transport hubs while rural and remote clinics lack refrigeration that makes farmers lose their hard earned produce to heat-spoilage. If cooling is essential infrastructure – as COP30 correctly stated – then equity must be its organising principle.

Fossil Fuels: The persistent gap between language and action

Perhaps the most telling outcome of COP30 was not what was agreed but what remained unresolved. Despite growing scientific and economic consensus, the conference stopped short of establishing a concrete, time-bound global roadmap for phasing down fossil fuel production. COP28, held in UAE, a country that continues to prosper due to its fossil fuel reserves, had managed to highlight the phase-out of fossil fuels for the first time ever in the history of COPs – and that, too, under the presidential leadership of H.E. Dr Sultan Ahmed Al Jaber, who is a member of the UAE Federal Cabinet, the Minister of Industry and Advanced Technology and, perhaps most tellingly, the Managing Director and Group CEO of the Abu Dhabi National Oil Company (ADNOC).

The language at COP30 reaffirmed previous commitments to “transition away” from fossil fuels, but without milestones, sectoral benchmarks or accountability mechanisms. This ambiguity is increasingly difficult to justify. The global clean energy investment now exceeds fossil fuel investment, and renewable technologies consistently outperform on cost and deployment with unprecedented speed. COP30 failed to send these market signals to the world.

The central deficit is accountability

At its core, COP30 highlighted a structural weakness that can no longer be ignored: Climate Governance relies on goodwill in a world where delay is often politically convenient. Countries that miss deadlines face no penalties. Finance pledges remain voluntary. Weak NDCs, not linked to the ambitious targets, carry no consequences. This system may have been adequate when climate change was perceived as a future risk; it is no longer fit for a world experiencing widespread compound climate shocks that keep knocking on our doors.

For industry leaders and governments alike, the lesson from Belém is not one of despair, due to betrayal, but a direction for determination.

Three shifts are essential:

From pledges to performance metrics Climate commitments must be assessed with the same rigour applied to public fiscal policy and industrial policy.

From ‘equity as rhetoric’ to ‘equity as actionable design principle’ Cooling, adaptation and energy transitions must explicitly prioritise vulnerable economies, food and health insecurity, not assume trickle-down benefits to the poor, and

From consensus to leadership coalitions Progress will increasingly come from groups of willing countries and companies moving faster and setting de facto global standards.

Though countries failed in their efforts, COP30 did not fail. But it did confirm that ‘progress’ framed only as ‘process’ is no longer sufficient. The world has crossed a threshold where climate outcomes are impacting economic stability, public health and geopolitical risk.

Let us also not forget the unstoppable surge that took place in renewables. For the first time in our history, the world now generates more electricity from renewables than from coal. Solar energy leads, and Mother Nature is back in business. Countries like China, India and some in the Middle East are not only taking positions but performing. China makes 80% of the world’s solar cells, 70% of windmills and 70% of lithium batteries. It dominates in hydropower. And as for India, 50% of the installed capacity of electrical energy in the country now comes from renewable sources. Indeed, it is a breakthrough, but it is not breaking the rising trend of GHG emissions.

Belém offered clarity, incremental finance progress, and important advances of intentions, such as the Global Cooling Pledge. What it did not deliver is the governance shift needed to match ambition with accountability for emission mitigation. For governments and industry, the message is clear: The next phase of climate action will not be judged by promises made at COPs and glossy reports on status but by bending the curve of rising emissions, measurable outcomes, equitable design and by the courage to move ahead even when consensus lags.

Dr Rajendra Shende is Former Director, UNEP, and Coordinating Lead Author of IPCC 2007, which won the Nobel Peace Prize. He is also the Founder of Green TERRE Foundation. He may be reached at shende.rajendra@gmail.com

Strategic planning can be a way to avoid interoperability problems, and AI ought to be an integral part of the initiative, say Dr M Ramaswamy and Bader Al Rashidi

According to the Oman Census Bureau Report, over USD 370 billion was invested in new facilities, facility renovations and additions in Oman in the year 2014. The figure excludes residential facilities; transportation infrastructure, such as bridges and roads; and facility operation and maintenance (O&M) costs.

The highest costs were incurred by owners and operators, and 85% of those costs were incurred during O&M. Annual interoperability costs of USD 15.8 billion were quantified for the capital facilities industry in 2012. The major cost was time spent finding and verifying facility and project information, which shows that extensive research is still needed to find out ways that can reduce the cost of O&M in building projects.

There exist nowadays two main challenges in intelligent building integration research. The first refers to overcoming the hindering factors imposed by the lack of interoperability amongst the building automation systems products from the multitude of available vendors. The second challenge is with regard to integrating building automation systems with the overall enterprise applications and, moreover, doing so over the Internet.

A large number of documents and drawings are generated within the design stage of a construction project. The rapid growth in the volume of project information, as the project progresses, makes it increasingly difficult to find, organise, access and maintain the information required by project users. The need for integration of this information is evident due to the numerous benefits it can bring to occupants of the building as well as the facilities operators/managers. Hence, strategic planning can be a way to avoid interoperability problems, which helps in defining open and universal standards for not only current facilities, but for any planned facilities in the foreseeable future.

It is in this long-term strategic planning, where Building Information Modelling (BIM) comes into the picture as a tool to be used for data handover. Efforts to provide more effective and efficient solutions to interoperability issues led to the adoption of open and standard communication protocols to provide uniformity to the communication process in all layers of interaction. Since 1995, initiatives such as the Industry Foundation Classes (IFC), developed by the International Alliance for Interoperability (IAI), have driven interoperability among software vendors who support the sharing and reuse of design, as-built and maintenance data on building projects.

Well-run BIM projects result in coordinated and consistent information about a facility, as it evolves through design and construction. The information, in the form of a BIM model, can by itself be used for O&M, without the need of the added step of data extraction. It is a known fact that the market of Facility Management (FM) is increasingly expanding, and efficient systems are necessary to support the Facility Manager’s decisions.

Facility managers usually manage maintenance and activities using systems that usually cause an inadequate monitoring of building management features. The introduction of BIM processes can improve the efficiency of building management, linking external databases to a virtual representation of a real estate. However, current research of BIM-based FM supporting systems shows some open issues, especially in the case of old buildings with a high number of daily users. Therefore, it is high time that the latest digital technologies be used to allow the development of integrated systems to support FM operations, providing several advantages in comparison to existing techniques and technologies. Hence an earnest attempt is made in this paper to study the feasibility of using Artificial Intelligence (AI) in FM.

AI and its benefits

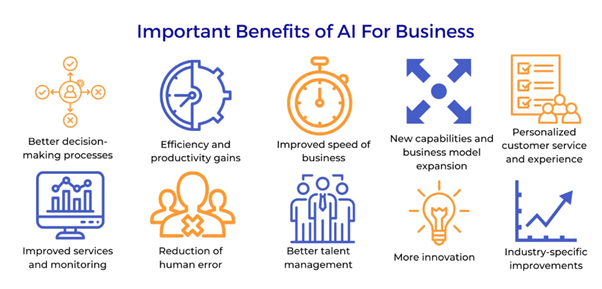

AI has rapidly evolved from a futuristic concept to a practical tool those businesses across various sectors leverage for competitive advantage. The integration of AI in business processes can enhance efficiency, drive innovation and create new opportunities for growth. In today’s rapidly evolving business landscape, the integration of AI has become a pivotal transformational force. AI, with its capability to analyse data, automate tasks and make intelligent decisions, has shifted the way organisations operate, compete and deliver value to their customers. Businesses are increasingly leveraging AI to gain a competitive edge and to address complex challenges. The role of AI in business processes is not limited to a single industry or function. It has the potential to transform operations across sectors, making them more efficient, customer-centric and data-driven. AI is not merely a technological trend but a fundamental shift in how businesses operate and compete. FM industries are evolving globally by adopting latest technologies. When these technologies are connected to an integrated workplace management system (IWMS), all of that data is consolidated into a single platform, and the FM manager can make better-informed decisions. FM companies aspire to deliver a Total Facility Management (TFM) solution, as shown in Figure 2, to clients, wherever possible.

Figure 1: Total Facility Management (TFM) solution

Challenges in various FM activities, such as managing failures efficiently, controlling costs, maintaining quality and automation, can be easily addressed by adopting AI technology in the FM domain. Figure 2 shows the role of AI in business in general.

Figure 2 AI in business in general

AI as a technology has been already in use in many industries:

Healthcare: AI is used for diagnostics, personalised medicine and robotic surgeries.

Finance: Includes fraud detection, algorithmic trading and personalised financial advice.

Transportation: Encompasses autonomous vehicles, traffic management and logistics.

Customer Service: Chatbots and virtual assistants provide support and handle queries.

Entertainment: Recommendation systems for movies, music and other content.

It is time for FM industries to adopt the use of AI in their business process. This paper is an attempt to facilitate the FM professionals to include the use of AI as one of the best professional practices.

Benefits from the implementation of AI AI plays a crucial role in analysing vast amounts of data quickly and accurately. It can identify patterns, trends and anomalies that might be challenging for humans to detect. This data-driven approach informs decision-making easier. The role of AI in FM (see Figure 3) is not limited to a single function. It has the potential to transform operations across sectors, making them more efficient, customer-centric and data-driven.

Figure 3: Important benefits of AI for any business

Strategy to introduce AI into FM business

A successful strategy should act as a roadmap to introduce AI into FM business domain and act as a driving mechanism to implement it. Depending on the organisation’s goals, the AI strategy might outline the steps to effectively use AI to extract deeper insights from data, enhance efficiency and build a better delivery process. A well-planned AI strategy should also guide the technological infrastructure, ensuring that the business is equipped with the hardware, software and other resources needed for effective AI implementation. Since technology evolves at a fast pace, the strategy should allow the organisation to adapt to new industry tools, frameworks and shifts.

It is an established fact that AI offers a vast array of capabilities with virtually limitless potential, including automating repetitive tasks, providing predictive insights, enabling personalised customer experiences, optimising supply chain management and improving risk assessment. A good strategy should use each of these capabilities to the best and meet the business mission of the FM domain. Implementing a successful AI strategy requires the following four pillars:

Data governance and management: Governance and management help to establish powerful data frameworks and implement effective data management practices to ensure the quality, integrity and security of data used for AI applications.

Technology and infrastructure: Building scalable and flexible technology infrastructure capable of supporting AI initiatives is very critical to the successful implementation of AI strategies. Infrastructure also includes data storage, computing resources and integration with existing systems.

Talent and skills development: AI strategies implemented in FM business will help to invest in acquiring and developing AI talent with the necessary skills and expertise to develop, deploy and maintain AI solutions effectively. Ethics, Security and Compliance: Generative AI is quite a new technology, so it is very important to stay informed about relevant regulations and standards governing AI usage in certain industries and ensure compliance with legal and regulatory requirements related to data privacy, security and ethics. It is also advised to prioritise ethical considerations in AI development and deployment, ensuring fairness, transparency, accountability and privacy protection in all AI-driven processes and decisions.

The step involved in implementing AI into business strategy is shown in Figure 4.

Key components of AI

Machine Learning (ML) is a subset of AI that involves training algorithms to learn from and make predictions or decisions based on data. Key methods include supervised learning, unsupervised learning and reinforcement learning. Natural Language Processing (NLP) enables machines to understand and respond to human language. Examples include chat bots and translation services. Computer Vision allows machines to interpret and make decisions based on visual input from the world, such as recognising objects in images or videos. Robotics combines AI with mechanical engineering to create autonomous machines capable of performing complex tasks, often in environments hazardous or inaccessible to humans. Expert Systems mimic the decision-making abilities of a human expert. These systems use a knowledge base and set rules to solve specific problems within a domain.

Based on the above, a well-defined strategy is required to introduce AI into the FM business. It needs experts in different specialties, like Information Technology and Computer Science and engineering. Generally, Facilities Managers are from the general engineering stream like mechanical or electrical; in the modern age, though, FM needs to be an inter-disciplinary approach.

Recommendations for implementation of AI in FM services

The future with Generative AI holds immense potential for revolutionising core activities in FM. Embracing the future of AI in FM looks promising. Leveraging Generative AI’s advanced capabilities can lead to unprecedented efficiency, cost savings and strategic advantages. The key to unlocking this potential lies in a robust, integrated data framework and a commitment to transparency and governance. Transparency and governance levels will likely vary by industry as well as task. There will likely be different levels of standards established – individual company standards, community standards, professional organisation standards and regulatory standards. Organisations may establish process committees to document acceptable levels of transparency and may require assurances from solution providers detailing information governance. Implementing AI in FM services requires a strategic approach that includes assessing needs, choosing the right tools, training staff and continuously optimising the system. The focus ought to be on areas like predictive maintenance, energy optimisation and space utilisation, where AI can deliver immediate value.

However, there are a few challenges to implementing AI in FM. They are:

Implementation costs: Integrating AI solutions can require significant upfront investment.

Data security and privacy: Ensuring the security and privacy of sensitive data is crucial when implementing AI solutions.

Integration with existing systems: Integrating AI with existing building management systems can be complex.

Change management: Adapting to new AI-powered processes and technologies requires a change management strategy.

Ethical considerations: Ensuring fairness and avoiding bias in AI algorithms is essential.

The use of AI in business across different industries revolves around ensuring optimal use of available data. Every business generates and works with massive amounts of data, which goes unnoticed. However, AI helps in capitalising on the data generated by businesses to provide a strong foundation that propels businesses towards the future.

AI is not merely a technological trend but a fundamental shift in how businesses operate and compete. It is a cornerstone in shaping the future of business processes, where data-driven, intelligent decision-making will be at the forefront of success.

In summary, the journey to fully realising AI’s potential in FM is just beginning, but this technology is too promising to wait for the dust to settle. Facility Managers need to engage in AI discussions and embrace the opportunity for improving FM.

Dr M Ramaswamy is with the Levels Training Institute, Oman. Bader Al Rashidi is with the Royal Court Affairs, Oman.

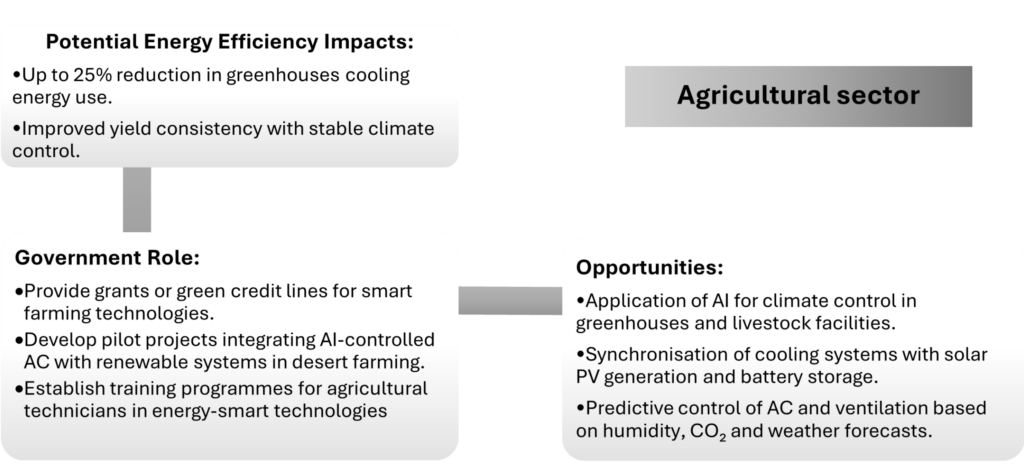

Demand Response programmes can unlock significant improvements in energy efficiency through AI-enabled smart control of air conditioning (AC) systems across diverse sectors, says Dr Angela Fandino of Engineering Sustainable Futures (ESF)

Dr Angela Fandino

Demand Response (DR) programmes can unlock significant improvements in energy efficiency through AI-enabled smart control of air conditioning (AC) systems across diverse sectors. DR facilitates dynamic adjustment of AC loads in response to grid conditions, real-time pricing, and the availability of renewable energy, thereby enhancing system flexibility and resilience.

Through targeted policies, incentives and regulatory frameworks, the UAE can accelerate DR adoption, unlock large-scale potential, and establish itself as a global leader in smart energy management and sustainable cooling.

AC systems account for up to 70% of total electricity demand during peak summer months in the UAE. This dependence on cooling creates significant stress on the power grid and results in high energy intensity per capita. To address this challenge, the integration of AI and smart control systems in AC technologies presents a strategic opportunity for improving energy efficiency, optimising DR and supporting national decarbonisation goals under the UAE Net Zero 2050 Strategy.

Smart AC controls utilise data-driven algorithms to predict demand patterns, optimise cooling schedules and adjust performance dynamically in response to user behaviour, occupancy and grid conditions. When integrated with DR frameworks, these technologies enable flexible, intelligent load management across all sectors of the economy.

Evidence

Smart Controls and AI Integration

Smart controls combine sensors, actuators and communication modules managed by AI algorithms that learn user behaviour and comfort preferences, predict indoor thermal dynamics and ambient temperature trends, communicate with utilities to respond to DR signals in real time and optimise energy use without compromising comfort or productivity.

Demand Response (DR)

Demand Response is a grid management mechanism in which consumers adjust their energy consumption in response to time-varying electricity prices, grid constraints or the availability of renewable energy.

AI enhances DR by enabling automated, predictive responses, coordinating load reduction during peak hours and increasing flexibility in integrating solar and other intermittent renewable sources.

AI fundamentally shifts DR from reactive curtailment to predictive, automated grid orchestration. It does so by combining Machine Learning, real-time analytics, forecasting and autonomous control systems.

DR has delivered clear, measurable results across mature electricity markets. In the United States, DR provides approximately 33,055 MW of capacity, equal to 6.5% of peak demand across Regional Transmission Organizations (RTOs) and Independent System Operators (ISOs). DR programmes delivered around 12,322 MW peak load reduction and 409 GWh annual energy savings in 2024. The USA-DOE residential pilots achieved 13-40% peak reductions per participant.

In the United Kingdom, the national Demand Flexibility Service reduced approximately 5.4 GWh in winter 2024/25, and the Capacity Market auctions increasingly procure DR around 4-9% of secure winter capacity awarded to demand-side resources.

In Australia, DR pilot portfolio delivered more than 200 MW of peak reduction capacity, and wholesale DR Mechanism has already dispatched 1,258 MWh of DR energy since 2021.

In the European Union, DR has delivered up to 12% peak reduction (≈8,300 MW) in Nordic markets, and DR-enabled projects will shift 4.4 GWh/year to off-peak, avoiding high-emission peaker plants.

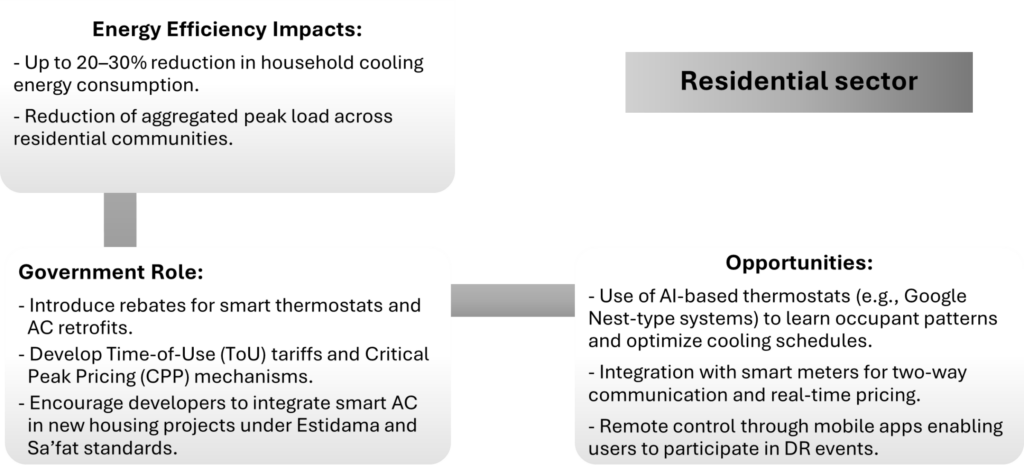

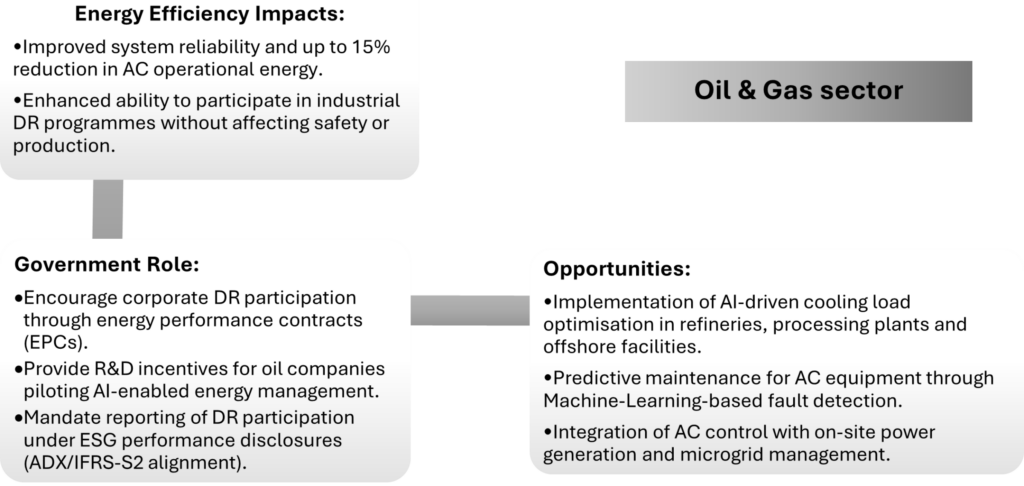

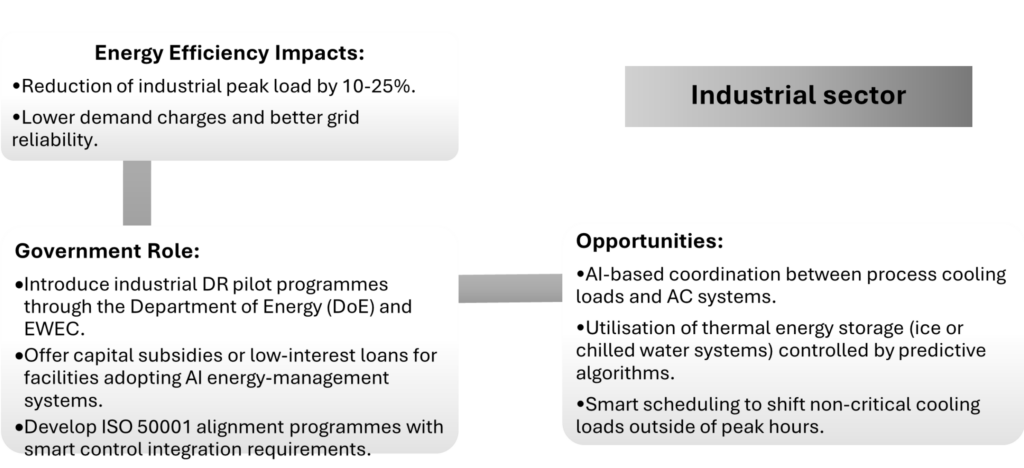

In the UAE, DR is now a formal target in Abu Dhabi’s energy policy, with contracted capacity goals of approximately 200 MW and scalability potential of up to 1,000 MW. Operational pilot data shows real DR capacity being delivered with measurable peak reductions and emissions avoidance. We can see that DR sits within a wider DSM 2030 framework, aiming for a 22% reduction in electricity use, which provides the systemic context for DR’s contributions.

At the national level, demand response is already reducing peak loads, avoiding costly generation investments and lowering emissions during peak supply periods.

Opportunities for energy efficiency

Here are the implications across sectors:

Sector

DR Opportunity

Benchmarks

Residential

Smart thermostats + TOU (time of use) tariffs

Large aggregated peak cooling reductions, similar to U.S. pilots achieving 13-40% peak reduction per participant.

Commercial buildings

Pre-cooling + automated controls

Peak load shifting and lower AC kW demand, reducing grid strain.

Industrial processes

Flexible scheduling + thermal inertia

Curtailment/load shifting in peak pricing hours.

Data centres

Cooling-load shifting + UPS (uninterruptible power supply) discharge

Similar to UK CM DR participation, substituting demand for generation.

District cooling

TES (thermal energy storage) charge/discharge alignment

Supports DSM’s 9% energy savings contribution through smarter operation.

Utilities/grid operators

DR resource participation

Defers capacity additions comparable to multi-GW avoided in EU/Nordic planning.

Residential sector

AI Enhances Demand Response in the Residential Sector

Key Flexible Loads

AI Capabilities Applied

Automated DR Actions

Peak Load Reduction Benefits

Renewable Integration Benefits

Strategic Value

Air conditioning, water heaters, EV chargers, appliances, rooftop solar PV systems & batteries

Government involvement through policies and incentives

Policy development

Policy Area

Description

Suggested Entity

Smart Control Standards

Develop national standards for AI-based AC control interoperability.

UAE Ministry of Industry & Advanced Technology (MoIAT)

Demand Response Regulation

Formalize DR frameworks allowing automated participation by all sectors.

DoE, UAE Ministry of Energy & Infrastructure (MOEI)

Green Building Codes

Mandate smart controls for new construction under Estidama, Sa’fat, and Dubai Green Building Regulations.

DMT, Dubai Municipality

Energy Data Sharing Policy

Ensure secure, anonymized data exchange between utilities and consumers.

TDRA, MOEI

Incentives and support mechanisms

Incentive Type

Mechanism

Beneficiary Sectors

Rebate Programmes

Rebates for installation of smart thermostats and sensors.

Residential, Commercial

Tax Deductions / Green Loans

Financial benefits for AI energy-management investments.

Industrial, Oil & Gas

Performance-Based Payments

Reward verified load reductions under DR events.

All sectors

Pilot Funding & R&D Support

Grants for AI DR demonstration projects.

Industrial, Agricultural

Training and Capacity Building

National skill programmes on AI energy management.

Technicians, engineers

Expected outcomes

Quantitative outcomes

Expected Outcome

Estimated Impact (UAE-wide by 2030)

Peak Load Reduction

5–10% of total grid demand

Energy Savings

15–25% of cooling electricity consumption

Carbon Emissions Reduction

Up to 8 MtCO₂e annually

Economic Benefits

AED 2–3 billion in avoided generation costs

Qualitative outcomes

Enhanced grid stability and renewable integration.

Improved consumer awareness and sustainable behaviour.

Strengthened ESG reporting and compliance across sectors.

Support for digital transformation and AI leadership within UAE Vision 2031.

These potential outcomes shall be verified through conducting gap analyses in the different sectors, taking into consideration national energy-efficiency and decarbonisation objectives, together with time-varying electricity prices, grid constraints and the availability of renewable energy.

Conclusion

DR is a proven tool, already delivering peak load reductions in mature markets, saving money and hundreds of GWh/year. The UAE’s DSM plus DR policies target material contributions by 2030, aligned with Net Zero 2050 ambitions and electricity reduction targets. Since cooling dominates UAE peak demand, DR applied through the optimisation of AC systems, TES, tariff reform and automation can unlock the majority of UAE’s near-term flexible capacity. The deployment of DR offers system-level economic value, deferring new gas-fired peakers and reducing network reinforcement requirements.

The implementation of AI-enabled smart controls in AC systems, when aligned with national DR strategies, represents a transformative opportunity for the UAE’s path toward a resilient, low-carbon energy future. Each sector, residential, oil and gas, industrial, and agricultural, stands to gain through energy savings, cost reduction and operational efficiency. By deploying targeted policies, incentives and regulatory frameworks, the UAE government can accelerate adoption, unlock large-scale DR potential and position the country as a global model in smart energy management and sustainable cooling innovation.

References

Abu Dhabi Department of Energy (DoE). (2023). Energy Efficiency and Demand Side Management Policy Framework. Abu Dhabi Government. https://www.doe.gov.ae

Abu Dhabi Energy Outlook 2050 – Department of Energy. https://doe.gov.ae

Al-Hammadi, H., & Al-Tunaiji, M. (2022). Smart Cooling and Energy Efficiency Strategies for the UAE Residential Sector. Renewable Energy and Sustainability Review, 46(4), 122–138.

Al-Sallami, A., & Alnuaimi, F. (2023). AI-Enabled Energy Management Systems in GCC Buildings: Demand Response Applications and Challenges. Energy Reports, 9(1), 456–471.

Demand Response Policy – Abu Dhabi Department of Energy. https://doe.gov.ae

Dubai Supreme Council of Energy (DSCE). (2022). Dubai Integrated Energy Strategy 2030.

Emirates Green Building Council (EmiratesGBC). (2021). Energy Efficiency Programmes and Smart Cooling Opportunities in the UAE. https://emiratesgbc.org

Emirates Water and Electricity Company (EWEC). (2022). Demand Side Management and Demand Response Programs in Abu Dhabi. https://www.ewec.ae

Estidama – Abu Dhabi Urban Planning Council. (2020). Pearl Building Rating System (PBRS) v1.0: Cooling and Energy Requirements.

Fandino Angela, Developing a Life Cycle Energy Model for Office Buildings, Sustainability-Engineering, Environmental Science, The University of Melbourne

Federal Energy Regulatory Commission 2024 Assessment of Demand Response and Advanced Metering (PDF). Federal Energy Regulatory Commission

Ghaddar, N., & Ghali, K. (2021). Artificial Intelligence in HVAC Control for Energy Efficiency and Thermal Comfort in Hot Climates. Applied Energy, 295, 117018.

International Electrotechnical Commission (IEC). (2021). IEC 60335-2-40: Household and Similar Electrical Appliances – Safety – Particular Requirements for Electrical Heat Pumps, Air Conditioners, and Dehumidifiers. Geneva: IEC.

International Finance Corporation (IFC). (2021). Energy Efficiency in Emerging Markets: AI, Digitalization, and Demand Response Mechanisms. Washington, DC: World Bank Group. https://www.ifc.org

International Renewable Energy Agency (IRENA). (2023). Innovation Outlook: Smart Electrification with Renewables. Abu Dhabi: IRENA. https://www.irena.org

ISO. (2018). ISO 50001:2018 – Energy Management Systems: Requirements with Guidance for Use. Geneva: International Organization for Standardization.

Reports on Demand Response and Advanced Metering – Federal Energy Regulatory Commission. Federal Energy Regulatory Commission

Sustainable Energy Development Authority (SEDA). (2022). Smart Grids and Demand Response Implementation Guidelines for Developing Countries. Kuala Lumpur: SEDA.

U.S. Department of Energy (DOE). (2022). Buildings Energy Data Book – HVAC Controls and Demand Response. Washington, DC: U.S. DOE.

UAE Federal Competitiveness and Statistics Centre (FCSC). (2023). UAE Energy Balance 2022 Report. https://fcsc.gov.ae

UAE Ministry of Energy and Infrastructure (MOEI). (2023). UAE Energy Strategy 2050 – Updated Vision and Roadmap. https://www.moei.gov.ae

United Nations Environment Programme (UNEP). (2022). Cooling Emissions and Policy Synthesis Report: Analysis and Recommendations for Policymakers. Nairobi: UNEP.

World Bank. (2023). Smart Cooling in Hot Climates: Sustainable HVAC Pathways in the Middle East and North Africa. Washington, DC. https://www.worldbank.org

The writer is Director, Energy and Sustainability at Engineering Sustainable Futures (ESF). She may be contacted at angela@esfmena.com

Premium Story

Policy, practice and the pursuit of decarbonisation

The 12th Edition of District Cooling Dialogue (“DC Dialogue”) in Riyadh brought stakeholders together to examine regulation, design maturity and innovation driving Saudi Arabia’s District Cooling sector

Held on October 7, 2025 in Riyadh, the 12th Edition of District Cooling Dialogue (“DC Dialogue”) conference reflected Saudi Arabia’s shift from exploration to structured acceleration in District Cooling. The event brought together government officials, developers, consultants, operators, manufacturers and other solution providers to examine regulation, technology, design governance and water policy as interconnected pillars of the Kingdom’s decarbonisation agenda.

The day opened with remarks acknowledging the purpose of the conference: To support the creation of a dynamic ecosystem for District Cooling aligned with Vision 2030.

Setting the tone for the day’s discussions, Salah Nezar, Senior Director of Design Management, New Murabba, delivered the Chair’s Overview. He reflected on four years of progress within Saudi Arabia’s District Cooling landscape and emphasised the need for synergy across refrigerant transition, water treatment, metering, smart controls and AI integration. Drawing on his AI-led optimisation work in the United States, Nezar encouraged the sector to “have the momentum to make a good component to the business,” reinforcing collaboration and cross-discipline alignment as prerequisites for further advancement.

This theme carried into the regulatory discussions. In his keynote, James Grinnell, Director, Water, Regulation and Supervision Bureau (RSB) Dubai, giving a UAE perspective, outlined how the Bureau’s remit has steadily expanded since its establishment in 2010 as a framework to attract private investment into cooling and energy services. He noted that the Dubai Supreme Council of Energy’s 2014 Demand Side Management (DSM) programme drew the RSB into several new areas, paving the way for legislation in 2021 that formalised its regulatory oversight of ESCOs, building energy management and efficiency monitoring. Grinnell explained that the Bureau’s work now spans efficiency accreditation, hydraulic system oversight and the monitoring of kilowatt-hour savings across both buildings and industrial facilities. He highlighted the importance of articulating why efficiency matters, both economically and operationally, to ensure that District Cooling remains a viable value proposition for investors, operators and consumers. This, he said, required transparent performance data and clear regulatory goals, particularly in a market split between air-cooled and water-cooled systems, where demonstrating measurable improvement was initially a significant challenge.

Regulations in Saudi Arabia – shaping policy, creating enabling mechanisms

The regulatory panel, moderated by Nezar, examined six interlinked areas shaping the pace of District Cooling adoption, including sustainability, incentives, mandates, regulatory clarity, investment structures and the industry’s general readiness. Nezar opened the discussion by questioning why District Cooling progress remains slow despite market demand and technical maturity, noting that design and regulatory processes continue to lag behind development ambition.

Nabil Shahin, Managing Director, AHRI MENA, underscored the national urgency behind accelerating District Cooling uptake. He pointed out that cooling accounts for 60-70% of Saudi Arabia’s electricity consumption, which places the sector at the centre of the Kingdom’s emissions-reduction commitments. District Cooling, he said, is particularly relevant for “high-density kilometres” and new-city developments, where the technology can serve as a primary tool for meeting national targets. Shahin also noted that Dubai’s trajectory, where companies are now exploring utility-like models, illustrates how strong regulatory direction can reshape market behaviour.

Grinnell reinforced the importance of clarity. He stressed that regulatory frameworks succeed when expectations are explicit and measurable, explaining that standards, such as those from ASHRAE, provide an anchor for ensuring systems “operate as efficiently as possible”. For operators as well as investors, he said, certainty is a critical enabler.

A recurring theme across the panel was the role of mandates and where they should be applied. Mohannad Khader, Commercial and Business Development Director, Diarona District Energy, argued that progress hinges more on enforcement than licensing. The industry, he said, needs targeted mandates, particularly in zones where District Cooling “makes sense” from both an economic and energy standpoint. Without them, the market risks fragmentation and inconsistent adoption.

Investment structure was another pressure point. Steve Lemoine, CEO – Middle East, Dalkia EDF Group, observed that PPP models remain underdeveloped in the Kingdom. While concession-style projects –such as those used in industrial clusters – offer a template, he emphasised that Saudi Arabia’s broader infrastructure priorities mean that PPP terms must become clearer and more predictable to attract the level of private capital required.

From a commercial perspective, Guillermo Martinez, Commercial Director, Araner, highlighted the challenges investors face when assessing proposals. Tariffs, payment structures and capacity-connection methodologies, he said, lack standardisation, making it “very difficult to compare one proposal to the other”. He stressed the need for transparent frameworks, noting that “capacity connection charts are not so easy for pricing”, and that clearer rules would help decision-makers evaluate competing technical and financial options.

Rounding out the discussion, Khalid A Al Mulhim, Managing Director and Sr. Engineering Consultant, Protecooling – Mulhim Design, urged caution and contextual awareness. Adoption, he said, must account for “the condition” of each site, operator capability and investor expectations. District Cooling decisions, he argued, should be made case by case, considering both technical and market-specific factors. “We have to put all the factors in respect,” he said.

Throughout the panel, Nezar underscored the importance of consistency, summarising that a streamlined approach with comparable proposals, coordinated regulation and aligned stakeholder expectations would allow the market to move in the right direction.

Developer perspectives and technological collaborations

The conversation then shifted to developer and consultant realities within large-scale projects. Again moderated by Nezar, the panel included Tamer Dahdouli, Project Associate Director, Diriyah Company; Abdul Zameer Ahamed Sab, MEP Lead (Principal), AtkinsRéalis; and Mohamed R. Zackariah, Chief Consultant, Mulhim Design, Protecooling.

Dahdouli highlighted the challenge of synchronising District Cooling plans with asset readiness. “The first or the pillar here is that these assets have to be ready, or their design has to be,” he said, noting that immature designs lead to misalignment downstream.

Ahamed Sab, giving a designer’s perspective, reflected on the transition from manual design methods to digital workflows, arguing that digitalisation requires structured processes, not just tools. Zackariah, also giving a designer’s perspective, added that collaboration between designers and contractors early in the project cycle is becoming essential to avoid on-site conflicts, especially in fast-paced giga-project environments.

Collectively, the panel underlined that improved design governance, disciplined workflows and shared data ecosystems are crucial for delivering reliable, scalable District Cooling across the Kingdom.

“Stronger control strategies”

Subsequently, Anas Alfar, Head of Product Consulting & Training, Hussain & Al Hassan G. Shaker Bros. For Modern Trading Co. LTD., which represents Midea in the Kingdom, gave the Industry Leadership Address. Outlining national targets to improve energy consumption by 30% by 2030, Alfar noted that District Cooling can play a significant role in achieving these goals, particularly through stronger control strategies. Alfar highlighted that Midea’s BMS platforms come with integrated monitoring as standard, providing “real, enquired data” that can be accessed remotely via web or mobile interfaces. He demonstrated how the platform offers detailed operational parameters rather than basic numerical snapshots, showing an example dashboard to illustrate the level of visibility available to operators.

The rise of autonomous buildings

Subsequently, Nezar gave a Special Address, during which he discussed the role of District Cooling within emerging smart-city ecosystems. Drawing on insights from the Barcelona Smart City Convention, he explained that global cities are increasingly integrating cooling, HVAC, lighting and other building systems into a single digital environment. Nezar emphasised that AI-driven optimisation is often unsuccessful when approached in isolation; instead, it requires a holistic framework that merges design expertise, operational understanding, system-wide data and coordinated controls. He noted that early AI projects in District Cooling have struggled precisely because partners “use the data, not from the system”, and stressed that defining the correct control frame is essential for AI to identify optimal operating conditions, as demonstrated in one of his own data centre projects.

A series of technical presentations that followed, deepened the discussion. Mina Sidhom, Sales Development Manager, Grundfos Saudi Arabia, outlined the company’s sustainability commitments, linking its work to global development goals on clean water, sanitation and climate action. He noted Grundfos’ initiatives to support NGOs in providing water access, and highlighted the organisation’s Eco-Lights Platinum rating, which benchmarks sustainability performance across multiple criteria.

Saudi Arabia’s ratification of the Kigali Amendment

Saeed Al-Lahham, Applied Development Leader, Trane, provided an overview of refrigerant evolution, explaining how the industry transitioned from legacy refrigerants, such as R-11, to lower-impact alternatives as global regulations phased out ozone-depleting substances.

Smart Buildings, Smarter HVAC

Roman Yerema, Head of Engineering, Belimo Automation FZE, shifted the discussion to controlled devices and energy performance, noting that buildings consume significant resources and that optimisation has become essential as energy costs rise. He explained that comfort delivery remains the primary objective, but historically, when energy was inexpensive, optimisation efforts were minimal.

Seawater energy recovery for District Cooling Closing the session, Cedric Carretero, Technical Director, Dalkia Middle East, presented seawater energy recovery as a complementary strategy for coastal developments. He explained that seawater can reduce freshwater dependency by eliminating the need for cooling towers, improve chiller performance and unlock additional efficiency benefits in buildings, an approach already adopted in various coastal regions, worldwide.

The TSE conundrum, alternative solutions

The final panel, moderated by Martinez, turned the spotlight to one of the sector’s most pressing issues: Examining Saudi Arabia’s water profile in the context of District Cooling. Comprising Celia Navarro, Business Development Engineer, Araner; Abdul Zameer Ahamed Sab, MEP Lead (Principal), AtkinsRéalis; Sidhom; and Zackariah, the panel dissected the “TSE conundrum” – the challenges and opportunities surrounding the use of Treated Sewage Effluent (TSE) in District Cooling.

Zackariah, reflected on the Kingdom’s earliest District Cooling work, noting that the first major project had mandated TSE use, which immediately raised questions about how the water should be applied. He explained that there has long been debate over whether TSE can be used directly with chillers or whether it requires an intermediate treatment stage. In practice, he said, the sector sometimes relies on temporary or inadequate measures, such as obtaining special permission to discharge into the civil network, highlighting gaps in quality control. Zackariah added that if power generation were to be fully decarbonised in the future, air-cooled systems could become a more viable alternative, easing pressure on water resources.

Martinez noted that the sector’s trajectory indicates a gradual shift towards wider use of TSE, underscoring its growing relevance in long term planning. From a supply perspective, Navarro stressed that availability alone is not the main issue. Treatment capacity and consistent quality are equally important. She observed that although significant volumes of TSE exist in theory, current treatment infrastructure may not be sufficient to support large-scale integration into District Cooling systems.

Offering a consultant’s perspective, Ahamed Sab explained that TSE performance depends heavily on cycles of concentration (CoC), which determine whether the water chemistry is compatible with cooling equipment. Clean water, he said, may achieve high CoC values, while untreated or variable quality TSE can limit system performance unless carefully managed.

Adding to this, Sidhom highlighted the importance of assessing water characteristics holistically rather than in isolation, given the operational risks associated with inconsistent supply or variable treatment quality.

Across the discussion, the panel agreed that while TSE presents significant opportunity, Saudi Arabia would benefit from a national water strategy that aligns supply, treatment capacity and system chemistry to support the sustainable growth of District Cooling.

The day closed with a reaffirmed commitment to a data-driven, transparent and collaborative future, where District Cooling leads Saudi Arabia’s urban decarbonisation while fostering economic growth and environmental stewardship. As the conversations drew to a close, a clear message emerged from the 12th Edition of DC Dialogue: Saudi Arabia is no longer in the exploratory phase of District Cooling – it is entering a period of structural acceleration. The day’s sessions underscored that regulation, digitalisation and water policy are not separate agendas but interconnected pillars of the same decarbonisation framework. Across panels and presentations, there was a shared understanding that District Cooling’s future lies in data-driven decision-making, interoperable systems and performance transparency.